WORKSITE INNOVATIONS INSURANCE GROUP

Benefit Strategies Built Around Your Business and Your People.

I'm Steven Swyers and I help Missouri business owners build benefits strategies that protect paychecks, improve access to care, and give you real control over long-term costs.

3-250

EMPLOYEE RANGE I SPECIALIZE IN

MO

LICENSED IN MISSOURI

WSI

REPRESENTING WORKSITE INNOVATIONS INSURANCE GROUP

365

DAYS A YEAR I STAY ENGAGED, NOT JUST AT RENEWAL

WHO I AM

An Advisor, Not A Vendor

I'm an independent benefits advisor based in Jefferson City, and I grew up in this work. I sit down with owners, HR teams, and individual employees across Central Missouri.

My job is simple to describe and harder to do well. Understand your situation, tell you the truth about what you already have, and build something that protects your people without wasting your money. I represent Worksite Innovations Insurance Group, and I stay involved all year, not just when renewal shows up.

I'm also a husband and a father of four children, so I think about this the way you do. What actually happens to a family when something goes wrong, and whether the coverage holds when it matters.

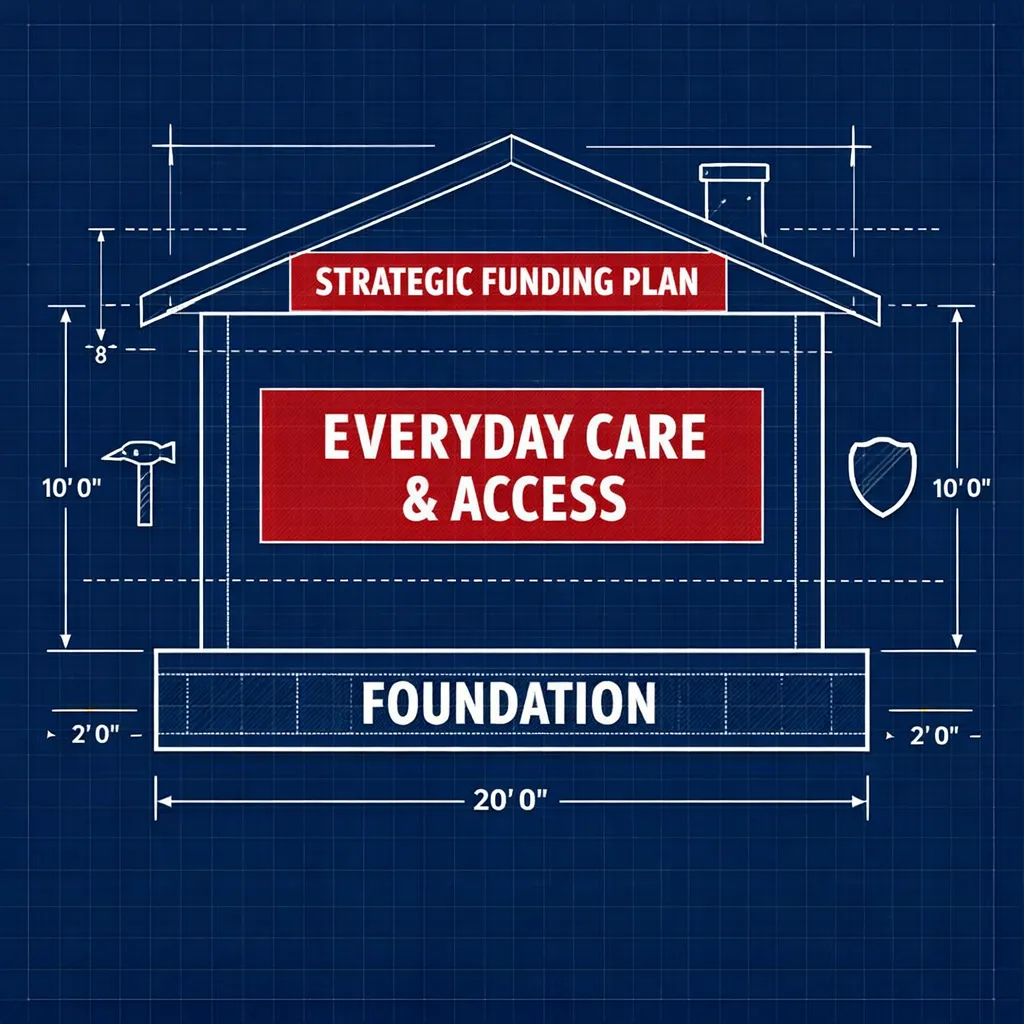

THE FRAMEWORK

Good benefits work like a well built house.

Every strong plan I build stacks the same way. Each layer does one job, and the whole thing only holds if it is built in the right order.

Roof

Major Medical Strategy

The right funding strategy for where your company is today, from traditional plans to self funding, matched to your real numbers instead of a generic quote.

Walls

Everyday Care Your Team Actually Uses

Direct primary care, virtual telehealth, dental, and vision. The coverage people reach for all year, not only in an emergency.

Foundation

Income protection underneath it all

Disability, accident, critical illness, and life. So one hard day for an employee does not turn into a crisis for your business.

WHAT I DO

What We Can Work On Together

I build benefits as a coordinated system, not a stack of products sold one at a time. Here is how the pieces fit together.

CORE

Major Medical Health Insurance

Most companies treat major medical as a fixed cost they renew and hope for the best on. I treat it as something you can actually see into and influence. We look at how your plan is really priced, how this year's claims shape next year's number, and which funding approach fits you, whether that is fully insured, level funded, or self funded.

The goal is a medical plan you understand and have some control over, instead of a bill that shows up every year with no explanation behind it.

ACCESS TO CARE

Direct Primary Care

A plan only matters if your team can actually use it. That is why I build around direct primary care, where employees get a real relationship with a physician, same or next day visits, and most of their everyday care for one flat monthly cost.

Paired with the right medical plan, it lowers what people pay out of pocket and keeps them from putting off care because of the price. Set up to be HSA-compatible, it works alongside a high-deductible plan without giving up the tax advantage. It is the difference between coverage that looks good on paper and care your team will actually use.

INCOME PROTECTION

Disability, Accident, Hospital + Critical Illness

Health coverage handles the medical bill. Income protection handles everything else, the paycheck, the mortgage, the part of life that does not pause when someone gets hurt or sick.

These are cash paying plans that go straight to your employee when they need them, and they pair with any health plan.

OPERATIONS + PLATFORMS

Platforms & Administration

Practical, competitive options that employees actually use and that fit within a thoughtfully structured total benefits package.

Good benefits fall apart when they are a mess to run. I bring the technology and the process that make a plan easy to manage: enrollment that connects to your payroll, a modern system for administering it all, help staying compliant, and clear education so your team understands what they have.

Less time answering benefits questions, fewer enrollment headaches, and coverage that actually gets used.

STATE OF MISSOURI EMPLOYEES

State Employee? You have a lane here too.

Alongside my work with companies, I handle voluntary benefits for State of Missouri employees. These are payroll deducted coverages you can add on your own to protect your income and your family, at group rates, with someone local to walk you through them.

If you are trying to figure out what to enroll in, or whether what you already have still fits, book a time and I will make it simple.

Voluntary Benefits Available For State Employees Through Payroll Deduction.

Short-Term Disability

Hospital Indemnity

Accident Expense

Dental

Whole Life Insurance

For complete plan details, click the button below.

PROCESS

How We Work Together

No long discovery processes. No vague timelines. Here is exactly what working together looks like.

Initial Call

A 30-minute conversation to understand your situation, what you currently have, and what you are trying to solve. No pressure, no presentation. Just a direct conversation to see if there is a fit.

Plan Review

I look at your current plan documents, contribution structure, and renewal history. If there are problems, I will tell you clearly what they are and how significant they are.

Strategy Presentation

I come back with specific recommendations, not a stack of carrier quotes. You will understand the reasoning behind every option I put in front of you.

Implementation

If you decide to move forward, I handle the transition. Carrier paperwork, enrollment setup, and employee communication are all part of what I do, not things I leave to you to figure out.

Ongoing Partnership

I stay engaged throughout the year. When renewal season arrives, you have someone who already knows your plan and your priorities. Not someone starting from scratch.

Questions Owners Usually Ask

What does it cost to work with you?

Every call and plan review is free. As your advisor I'm compensated the way benefits advisors typically are, built into the plans rather than billed to you on top. I'll always be transparent about how any recommendation is structured before you decide anything.

Do I have to switch carriers or blow up my current plan?

Not at all! Sometimes the right move is a few adjustments to what you already have. I'll tell you the truth about your current plan first, and if it's working well, I'll say so.

How is this different from my current broker?

Most brokers appear at renewal with a stack of quotes. I build a coordinated strategy, explain the reasoning behind every option, and stay engaged all year, so you're never starting from scratch when something actually matters.

How much of my time will this take?

The first call is about thirty minutes. From there I do the heavy lifting, reviewing documents, building the strategy, handling implementation. Your team stays focused on running the business.

We're a small team. Are we too small to bother with?

Not at all. I specialize in Missouri employers from 3 to 250 employees. Smaller teams often have the most to gain from a plan that was actually built for them instead of handed down.

What exactly is direct primary care?

A flat monthly membership that gives your employees a real relationship with a physician, same or next-day visits and most everyday care included, without a copay at the door. It pairs with a high-deductible plan and stays HSA-compatible, which usually lowers total cost while making care easier to actually get.

Steven Swyers

EMPLOYEE BENEFITS CONSULTANT

REPRESENTING WORKSITE INNOVATIONS INSURANCE GROUP

CELL 573-415-8468 · OFFICE 888-339-3593 · [email protected]

© 2026 Steven Swyers LLC. All Rights Reserved.

This site is for informational purposes only and does not constitute an offer of insurance. Coverage is subject to plan terms, eligibility, and carrier approval. Steven Swyers is a licensed insurance advisor in the State of Missouri representing Worksite Innovations Insurance Group.